Commodities Wrap: Risk appetite supported by expectations of limited escalation in Middle East

Friday 10 July, 2026

Summary

Energy fell on expectations of limited escalation in the Middle East conflict. Precious and industrial metals gained amid a broad pick up in risk appetite.

Prices and commentary accurate as of 07:00 Sydney/05:00 Singapore/17:00(-1d) New York/22:00(-1d) London.

Ahead Today

Public holidays: None

Central bank speakers: ECB Vice President Boris Vujcic; ECB Governing Council member Yannis Stournaras

Economic data: Brazil – CPI; Canada – unemployment, building permits; France – CPI; Germany – CPI; Italy – industrial production; Japan – PPI; Mexico – industrial production; Poland – central bank minutes; Russia – CPI; Turkey – industrial production

Commodities reports: IEA Monthly Oil Market Report (UK 10:00am / NY 5:00am / AEDT 8:00pm); Shanghai Futures Exchange weekly commodities inventories (local release); Baker Hughes weekly rig count (NY 1:00pm / UK 6:00pm / AEDT 5:00am 11 Jul); CFTC Commitment of Traders (NY 3:30pm / UK 8:30pm / AEDT 7:30am 11 Jul); ICE Futures Europe Commitment of Traders (UK 6:30pm / NY 1:30pm / AEDT 4:30am 11 Jul); ICE gasoil July futures expiry

Events: ECOFIN meeting in Brussels; African Economic Conference begins in Abidjan; South African President Cyril Ramaphosa begins France visit; Saudi Arabia and Serbia sovereign rating reviews

Market data: Delta Air Lines 2Q earnings; SK Hynix ADR Nasdaq debut

Listen to today’s 5in5 with ANZ podcast for more on the global economy and markets.

Market Commentary

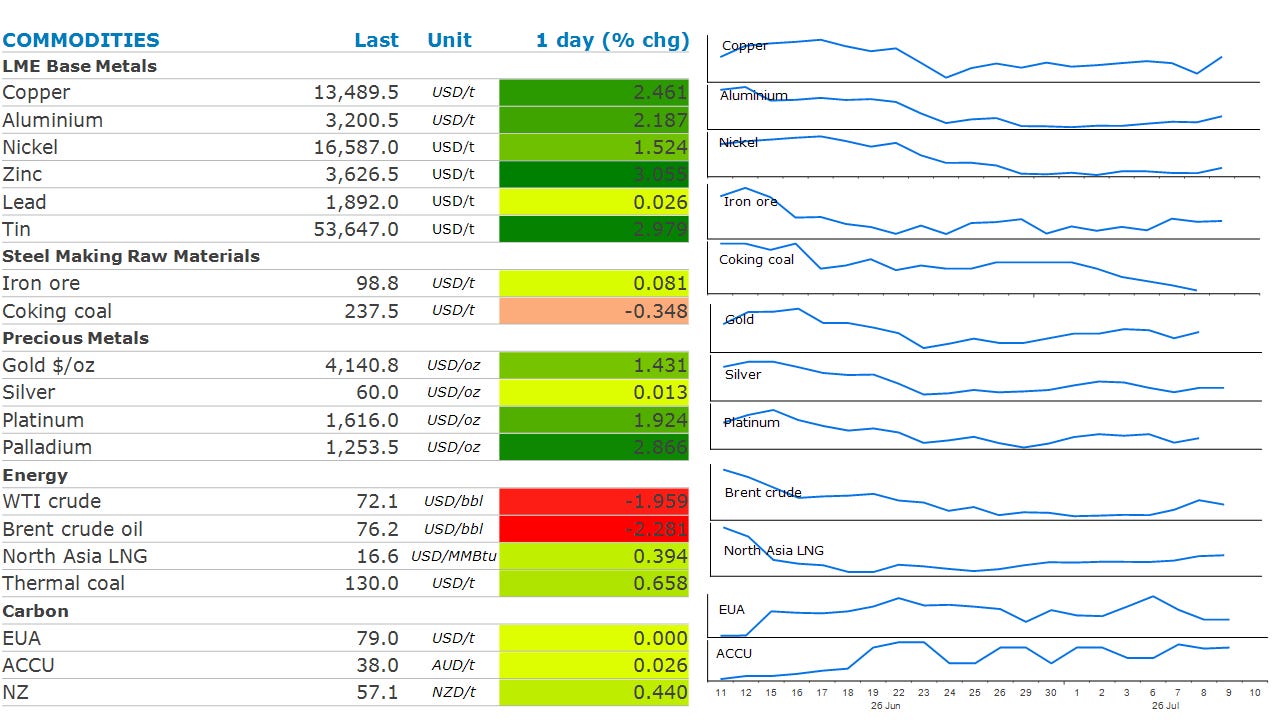

Crude oil prices ended the session lower amid expectations of limited military attacks between the US and Iran. Despite the US ramping up attacks on military sites in Iran, the market drew some reassurance from the Trump administration’s decision to avoid targeting Iranian energy infrastructure. This was aided by comments from President Trump, who said he doesn’t expect a return to a full-scale conflict. Nevertheless, traffic through the Strait of Hormuz remained severely restricted as the two sides exchanged strikes that were some of the heaviest since reaching a ceasefire agreement last month. Observable movements largely occurred along an Iran-approved route nearer to the waterway’s north. The US-supported Omani corridor was relatively quiet. The shipping industry has shown a reluctance to return to the Persian Gulf. Bloomberg reported that several owners of ships that had recently crossed the strait were still assessing whether it is safe to return. London marine insurers are seeing fewer inquiries for journeys through the strait. However, media reports suggest Iran has been able to rush out tankers carrying roughly 11mbbl of crude oil in the past 24 hours, after the fighting with the US resumed.

European natural gas prices pushed higher after reports that Qatar is pausing its efforts to rapidly revive production. This comes after an attack on one of its tankers in Hormuz raised concerns that transits through the key waterway remain too risky. QatarEnergy said that operations at its Ras Laffan plant will instead be kept at a minimum for safety reasons. and the number of vessels scheduled to dock at the plant in the coming days will be reduced. This threatens to further tighten the global gas market just as Europe needs to ramp up refilling of its storage facilities. They are currently only about 51% full and need to be near 90% by November. The change of plans in Qatar also raised concerns in the Asian LNG market. North Asia LNG prices have risen almost 10% over the past week and are now more than 80% above pre-conflict levels at USD18.5/MMBtu. Further disruption to supply from the Persian Gulf is likely to see competition for existing cargo ramp up. Pakistan has been particularly active, seeking cargo for July delivery.

Iron ore futures rose amid concerns of tightening supply. Reuters reported that hundreds of workers at BHP’s Port Hedland iron ore operations in Western Australia are threatening to walk off the job next week. The unions have called for an eight-hour work stoppage on 16 July, after six months of negotiations failed to reach an agreement on a four-year labour deal.

The base metals sector shrugged off the rising geopolitical risk to end the session higher. Copper led the gains amid the broader improved risk appetite amongst traders. It has also been supported by a slew of fundamental drivers. Inventories in China have recorded some large falls over the past week. There have also been some supply headwinds in South America. Zinc rallied more than 3% after reports of a fire at a major zinc smelter in South Korea operated by Young Poong Corporation.

Gold found some support on expectations of limited escalation in the Middle East conflict. This is despite earlier concerns that a rebound in energy prices could see the Fed keeping interest rates higher for longer to combat stubbornly high inflation.

Chart of the Day

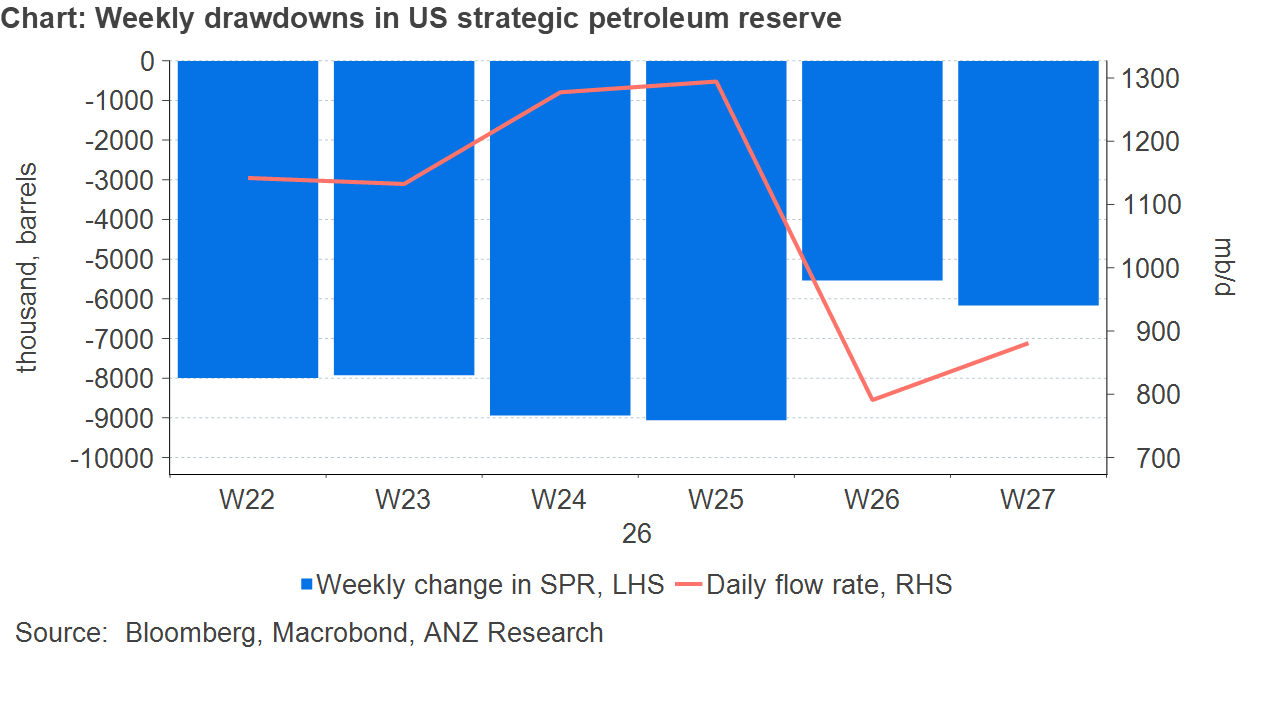

The broader drawdown in inventories continues despite this week’s EIA report showing commercial inventories rose 3mbbls. The US Strategic Petroleum Reserve has been the main source of supply since the Middle East conflict knocked out a significant amount of Persian Gulf output. Last week saw another 6.1mbbls released, This saw the run rate of the drawdown rise slightly to 900kb/d.

5in5 with ANZ Podcast