Commodities Wrap: Peace deal prospect pushes energy markets lower

Monday 25 May, 2026

Summary

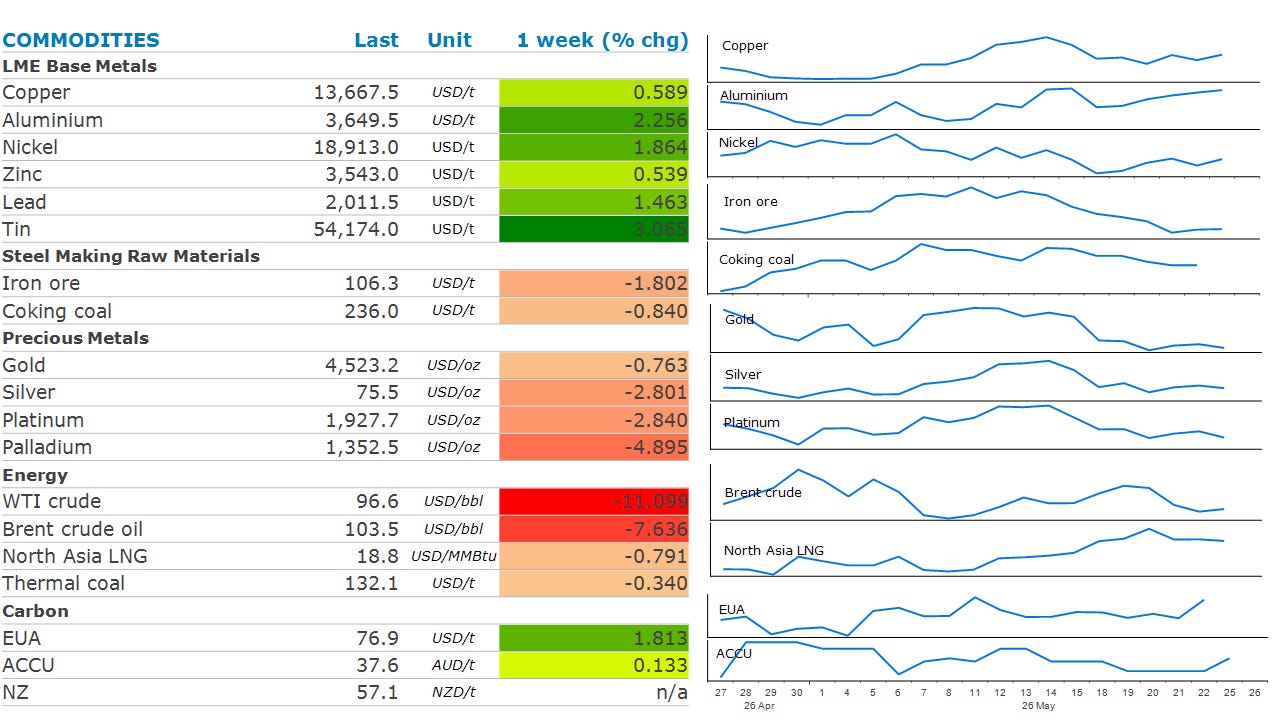

The energy sector fell last week on prospects of a US-Iran deal. Industrial metals gained amid a risk-on tone. Gold eased lower on hawkish comments from the Fed.

Prices and commentary accurate as of 07:00 Sydney/05:00 Singapore/17:00(-1d) New York/22:00(-1d) London.

Ahead Today

Public holidays: US Memorial Day; UK Spring Bank Holiday; South Korea; Hong Kong; Norway; Saudi Arabia

Central bank speakers: Chicago Fed President Austan Goolsbee (podcast appearance)

Economic data: Israel – rate decision; Mexico – trade; Nigeria – GDP; Singapore – GDP, CPI; Thailand – customs trade

Commodities reports: None

Events: Hajj pilgrimage begins in Mecca; Anthropic co‑founder Christopher Olah at Vatican AI encyclical launch; CME holiday schedule; ICE holiday schedule; KazMunayGas 1Q earnings

Market data: None

Listen to today’s 5in5 with ANZ podcast for more on the global economy and markets.

Market Commentary

Crude oil prices fell last week, as the market pondered a peace deal between the US and Iran that could ultimately reopen the Strait of Hormuz. Pakistan’s army chief headed to Iran to join talks that have been showing signs of progress. Iran said that the latest proposal from the US had partly bridged the gap between the two sides. However, the Islamic Republic’s supreme leader triggered some doubt after he issued a directive that the country’s near-weapons grade uranium should not be sent abroad, a key demand from the US. Iran was also working with Oman to setup a form of permanent toll that would formalise Iran’s control over maritime traffic through the Strait of Hormuz.

The effective closure of the strait continues to keep a significant amount of oil off the market. Abu Dhabi National Oil Co said Middle East oil flows would not fully recover until well into 2027, even if the conflict ended immediately. In the meantime, inventories are being drawn down sharply. US crude oil inventories plunged by a record 17.8mbbl last week. The US has also continued to strictly enforce its blockade of Iranian ports. The country’s navy said it had redirected 100 commercial vessels over the past six weeks. That could see Iran’s exports fall further over coming weeks. Meanwhile, refining margins, especially for distillates such as diesel and jet fuel, remain elevated, signalling persistent product tightness and suggesting the shock is being absorbed more by refined products.

Global gas markets were mixed as the closure of the strait has differing regional impacts. North Asia LNG prices ended the week higher as some buyers in the region dipped their toes back into the spot market. There are concerns that rising temperatures will boost gas demand as supply shortages build. This could be impacted by potential planned labour strikes by LNG workers at Inpex’s Ichthys LNG plant in Australia. In Malaysia, two production trains at the Bintulu LNG plant have been taken offline due to operational issues. European natural gas futures ended the week lower, as traders concerns over supply shortages eased on hopes of a US-Iran peace deal. This comes as its restocking requirements are less critical than those in Asia.

The risk-on tone across markets helped boost sentiment in the base metals markets. Copper found some support from a strong rally in computer chip manufacturers on Chinese stock markets. This raised hopes that demand for metals critical to the AI investment boom would rise. Nickel led the base metals complex higher, as concerns of further supply cuts in Indonesia emerged. Shanghai Metals Market reported that 10–15% of high-grade nickel pig iron capacity at the Weda Bay Industrial Park in Indonesia will be placed under maintenance in the coming months. Adding to this, Indonesia’s officials announced plans to tighten control over commodity exports, including coal and palm oil. Such government controls have led to dislocation of commodity markets in the past.

Gold edged lower, as traders’ expectations that the Fed will raise interest rates increased. This came after Waller warned that the US-Iran conflict’s energy shock could fuel inflation. Markets have now fully priced a quarter point rate hike by December for the first time. Meanwhile, US consumer confidence fell in May to a record lower, and long-term inflation expectations worsened notably, likely due to the conflict.

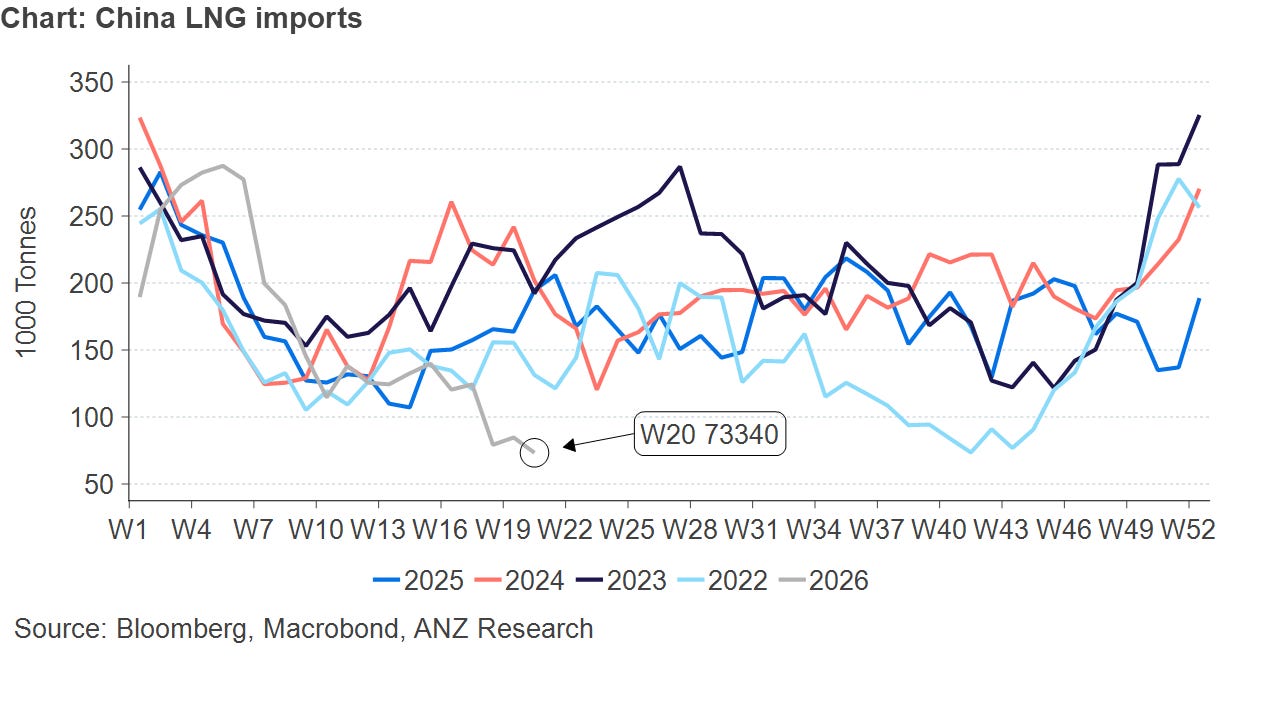

Chart of the Day

Panic buying in the global LNG market has been mitigated by a pull back in buying from China. In week 20, China imported only 73.3mt, far below its normal level of between 150-250mt at this time of the year. However, this is unlikely to remain the case for too much longer. As temperatures rise, higher gas fired power demand could force China to resume normal level of imports of LNG.

5in5 with ANZ Podcast