Commodities Wrap: Oil unchanged as rising crude supply meets product tightness

Tuesday 7 July, 2026

Summary

Moves were limited across the commodity complex. The energy and bulk sectors edged lower on rising supply. Precious metals fell on signs of weak demand.

Prices and commentary accurate as of 07:00 Sydney/05:00 Singapore/17:00(-1d) New York/22:00(-1d) London.

Ahead Today

Public holidays: None

Central bank speakers: ECB Governing Council member Fabio Panetta; ECB Governing Council member Martin Kocher

Economic data: China – foreign reserves; Colombia – CPI; France – trade; Germany – industrial production; Japan – leading index, labour cash earnings; Mexico – international reserves, vehicle production; Philippines – CPI; Taiwan – CPI; US – trade balance, ADP employment change (NY 8:15am / UK 1:15pm / AEDT 12:15am 8 Jul)

Commodities reports: EIA Short-Term Energy Outlook (NY 12:00pm / UK 5:00pm / AEDT 4:00am 8 Jul); API weekly US oil inventories (NY 4:30pm / UK 9:30pm / AEDT 8:30am 8 Jul)

Events: NATO Summit begins in Ankara (through 8 Jul); IETA Asia Climate Summit begins in Hong Kong (through 9 Jul); Nigeria Oil & Gas Energy Week continues; BOE Financial Stability Report; USTR hearing on forced-labour import enforcement; Allen & Co Sun Valley conference begins; French Court of Appeal ruling on Marine Le Pen challenge; SpaceX added to Nasdaq 100

Market data: Shell 2Q trading update

Listen to today’s 5in5 with ANZ podcast for more on the global economy and markets.

Market Commentary

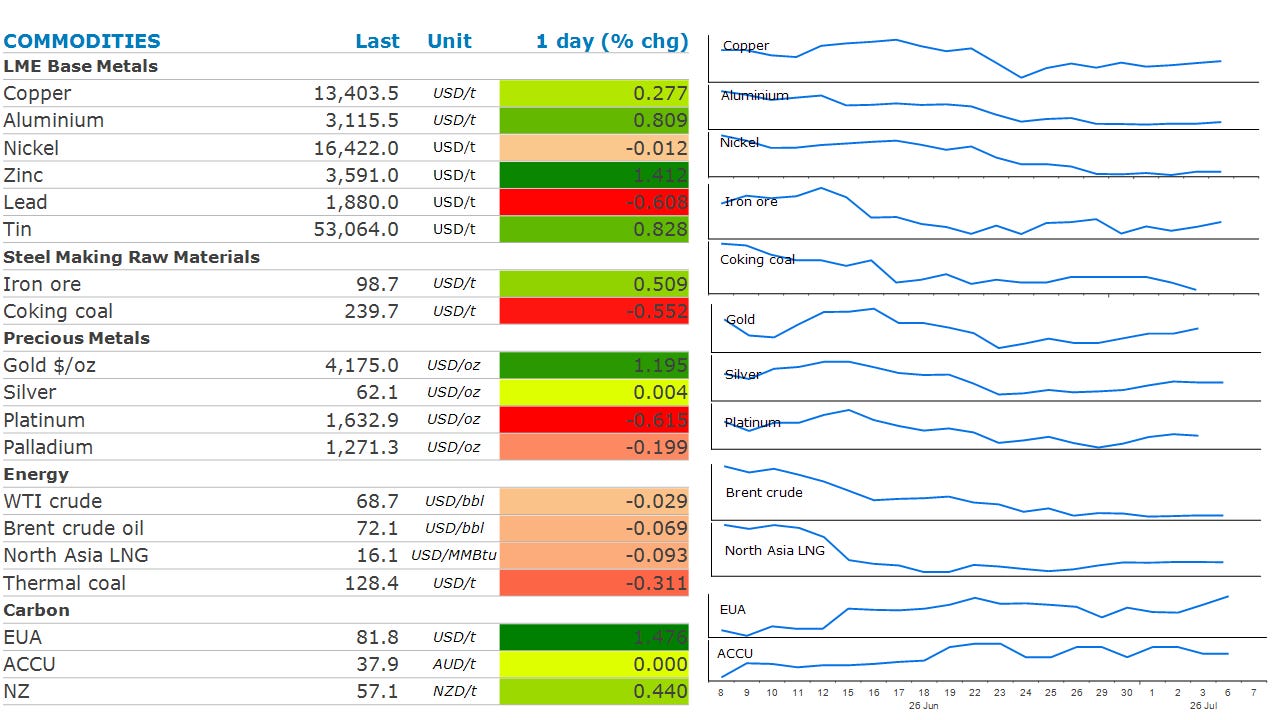

Crude oil prices switched between gains and losses as rising supply from the Persian Gulf offset ongoing tightness in product markets. Saudi Arabia has made big reductions to its main crude oil for buyers in Asia, selling barrels at a discount to the regional benchmark Arab light crude for the first time since 2020. This highlights the increase competition in the region following the surge in oil leaving the Persian Gulf in recent weeks. However, the market is still showing signs of tightness. Oil product markets remain significantly tighter than crude markets. Refining margins continue to strengthen, particularly in the US, as robust fuel demand collides with lean inventories and constrained product supply. Gasoline inventories are still drawing down while distillate and jet fuel stocks have only recently stabilised, creating ongoing support for crack spreads despite crude prices retreating to pre-conflict levels. And despite the recent surge in activity in the Strait of Hormuz, the recovery in oil flows is proving slower than expected. The initial rebound in tanker transits through the Strait of Hormuz has stalled, with vessel crossings remaining in single digits and no sustained recovery evident. While the interim US-Iran agreement has reduced immediate geopolitical risks, shipping operators remain cautious, limiting the speed at which crude exports can return to normal levels.

Asian LNG prices inched lower on signs of rising supply. The 30-day moving average of shipments from Australia rose to 229kt on Sunday, the highest level since late March, according to ship tracking data. This may provide some relief for markets still reeling from disruptions to supplies from the Middle East. Major Gulf producer Qatar has said its plans to ramp up LNG exports within weeks, but it has also recently extended force majeure on some shipments to Asia and Europe.

Gold prices inched lower as the market contemplates the outlook for interest rates. Swap traders are still pricing-in a 25% chance of the Fed hiking rates at its next meeting. However, this pricing has eased lower following data which showed a weaker-than-expected labour market. A fall in demand for jewellery has also weighed on sentiment. The World Gold Council estimates that global jewellery demand fell 23% y/y in Q1 2026 as high prices weighed on sales. This was driven by falls in China (-32%) and India (-19%).

Iron ore futures edged higher as concerns over tightening supplies continued to hang over the market. China’s state-backed iron ore trader, China Mineral Resources Group, is said to have expanded its curbs on Australian iron ore. The group has asked several domestic steel mills not to buy any USD denominated cargoes of Fortescue’s super special fines product. This helped offset the impacts of a seasonal slowdown in Chinese demand and small profit margins at Chinese mills, which have been squeeze by high coking coal prices.

Aluminium led the base metals sector higher, rising from a four-month low as some doubt over the resumption of exports from the Persian Gulf emerged. Last week, Emirates Global Aluminium said it aims to speed up resumption of output at its Abu Dhabi facility that was damaged during the US-Iran conflict. It said it’s working to reach full production of hot metal at the smelter earlier than the one-year timeline it previously reported. However, in the meantime the full reopening of the Strait of Hormuz remains elusive. Daily transits have risen but remain significantly below the pre-conflict level.

Chart of the Day

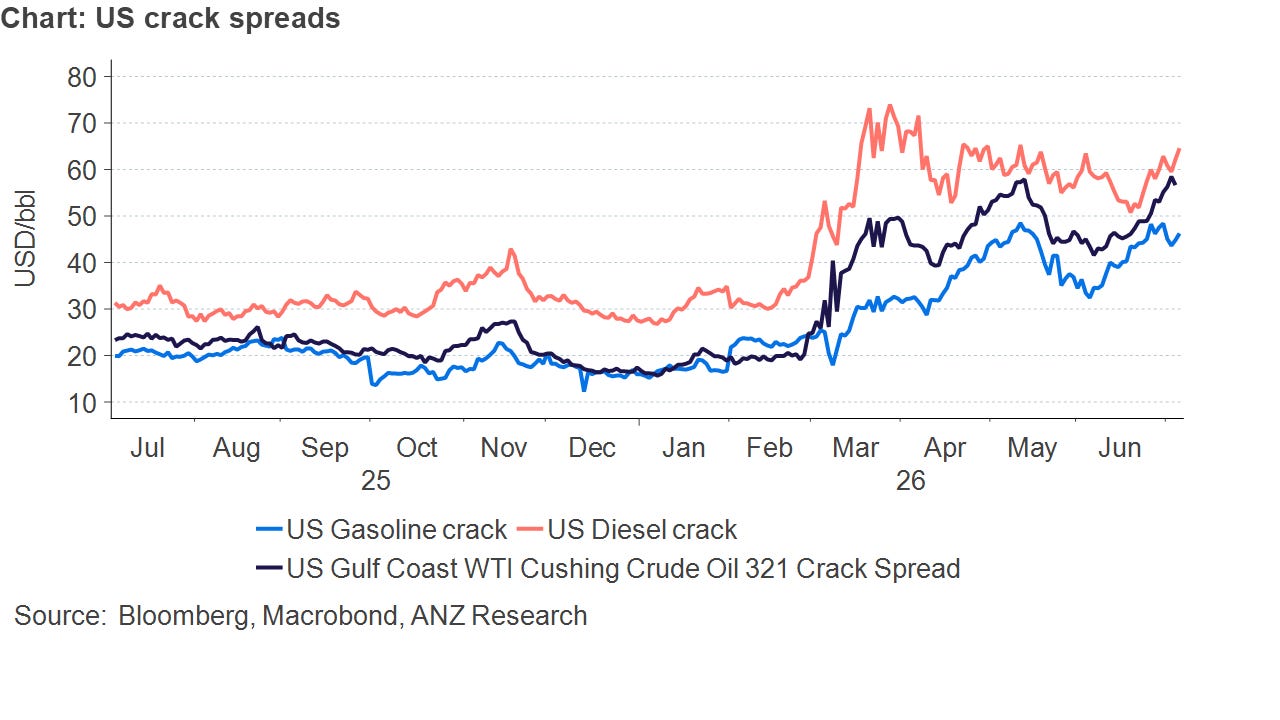

Refining margins in the US are rising sharply as product fuel markets remain tight. The immediate driver has been strength in gasoline markets. Gasoline cracks have risen to their highest levels since the onset of the Middle East conflict in late February, supported by a combination of low inventories and strong seasonal demand. With US refineries already operating at high utilisation rates, the system has had limited capacity to respond to this demand surge, amplifying upward pressure on margins. At the same time, refiners have been forced to balance competing incentives across the barrel, particularly the strong economics for jet fuel production, which has diverted yields away from gasoline and contributed to tighter balances

5in5 with ANZ Podcast