Commodities Wrap: Oil stabilises has market awaits signing of US-Iran deal

Thursday 18 June, 2026

Summary

The energy sector pushed lower amid a concern of a flood of supply. Precious metals slumped on a hawkish tone from the Federal Reserve.

Prices and commentary accurate as of 07:00 Sydney/05:00 Singapore/17:00(-1d) New York/22:00(-1d) London.

Ahead Today

Public holidays: Egypt

Central bank speakers: SNB Schlegel press conference; ECB Kocher Vienna; Denmark CB Thomsen

Economic data: Czech rate decision; Indonesia rate decision; New Zealand GDP; Norway rate decision; Philippines rate decision; Switzerland rate decision; Taiwan rate decision; UK BOE rate decision (12:00 London / 07:00 NY / 21:00 AEDT); UK jobless claims, unemployment; US initial claims (08:30 NY / 13:30 UK / 22:30 AEDT), leading index (10:00 NY / 15:00 UK / 00:00 AEDT), cross border investment; Ukraine rate decision

Commodities reports: OPEC World Oil Outlook; EIA weekly gas inventories (10:30 NY / 15:30 UK / 00:30 AEDT); Singapore oil product stockpiles; Insights Global ARA inventories; China base metals and oil product output; China trade (oil products, LNG, pipeline gas)

Events: European Council (through 19 Jun); NATO defence ministers Brussels; Africa Energy Forum continues; FT Climate & Impact Summit London (final day); BNEF Forum Seoul; UK by election; Ramstein Group meeting

Market data: Baker Hughes rig count (13:00 NY / 18:00 UK / 03:00 AEDT); WTI July CSO expiry

Listen to today’s 5in5 with ANZ podcast for more on the global economy and markets.

Market Commentary

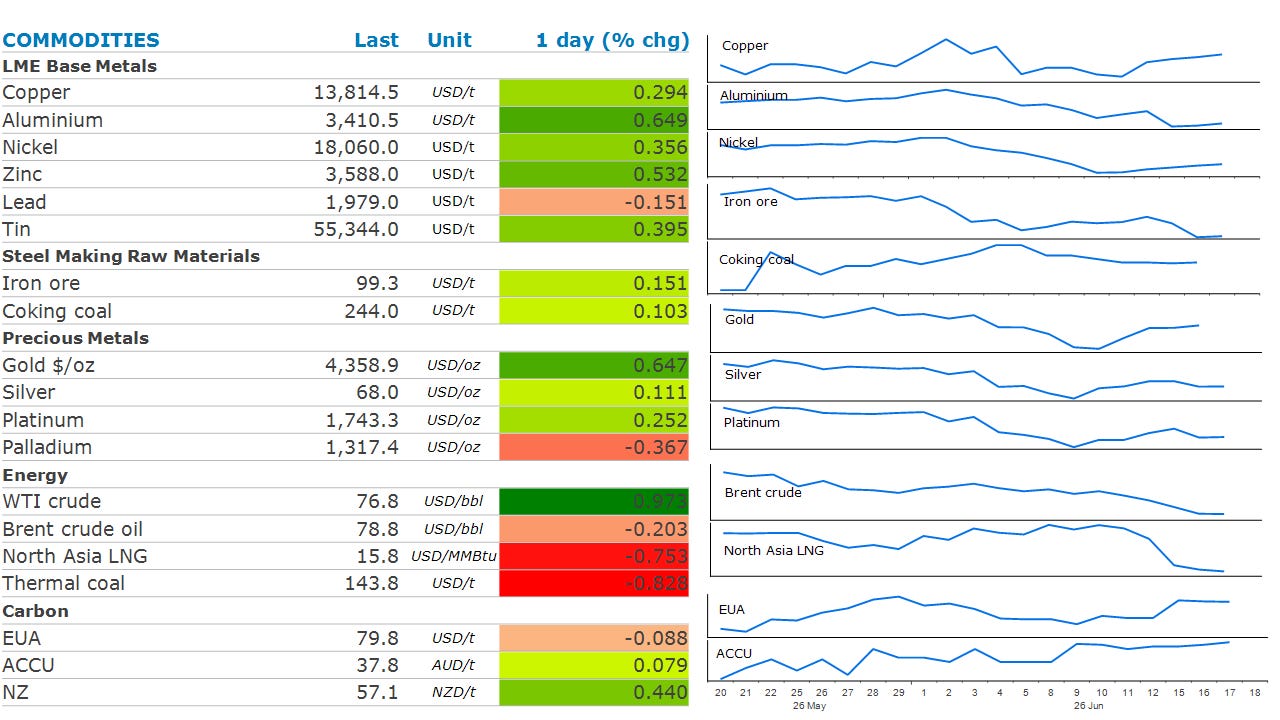

Crude oil prices stabilised as the market awaits more details on the US-Iran interim peace deal. A draft version reportedly circulating foresees an immediate reopening of the Strait of Hormuz, along with immediate sanction waivers for Iranian oil. That has sparked concern that a flood of oil will hit the market. However, there are considerable risks to this scenario. There remain concerns that shipowners will be reluctant to send oil tankers back into the Persian Gulf while there is a risk that the deal falls over. Then there is the clean up of sea mines that could take weeks or months to complete. In the meantime, the market continues to rely on lower demand and inventories to keep its balance. Oil stockpiles in the US saw another sharp drawdown last week. Commercial inventories fell by 8,263kbbl. At Cushing, the largest commercial storage in the US, inventories stand at only 20mbbl, equivalent to less than two days of US crude production. This is considered an operational minimum.

Sentiment wasn’t helped by more bearish forecasts. The International Energy Agency said that a glut of oil will emerge next year if the peace deal in the Middle East holds. Following a 900kb/d deficit in 2026, it expects a sizeable 5mb/d surplus in 2027. This is being driven by a rise in production of around 8mb/d to 110mb/d, far ahead of a “relatively modest” 2mb/d rise in global oil demand.

Global gas prices were also marginally lower as traders monitor the situation in the Middle East. European benchmark natural gas moved between gains and losses after the US and Iran committed to reopening the Strait of Hormuz. With the market still expected to remain tight as supply struggles to recover, concerns are centred around efforts to refill fuel stockpiles ahead of the northern hemisphere winter. North Asia LNG prices were lower, although the losses have sparked an increase in activity in the spot market from price sensitive buyers. Importers from Bangladesh, India and Pakistan have put out tenders seeking spot cargoes. China’s natural gas output fell in May by 2.2% y/y, raising concern that it may also need to increase purchases on the international market.

Iron ore fell below USD100/t for the first time since March on signs of stronger supply. Exports from Guinea’s Simandou iron ore project surged in May, six months after its first shipment to China. Volumes hit 2.2mt in the month, according to ship tracking data. That’s up from 1.3mt in April. Simandou is expected to produce around 120mt per year once fully commissioned. This comes following relatively weak economic data from China. Fixed asset investment for January–May came in below expectations, down 4.1% y/y. This subsequently triggered a fall in China’s crude steel output to 84.36mt (-2.7% y/y). Iron ore may also have been undermined by the slump in crude oil prices, with the subsequently weaker freight rates putting pressure on delivered prices into China.

The base metals sector was broadly higher amid an improved risk appetite for risky asset classes from investors. Supply side issues outside of the Middle East also provided support. Protestors blocked copper exports from the Oyu Tolgoi mine in Mongolia, which is crucial to China’s renewable energy ambitions.

Gold prices tumbled after Fed officials left interest rate unchanged while signalling the possibility of higher rates later this year.

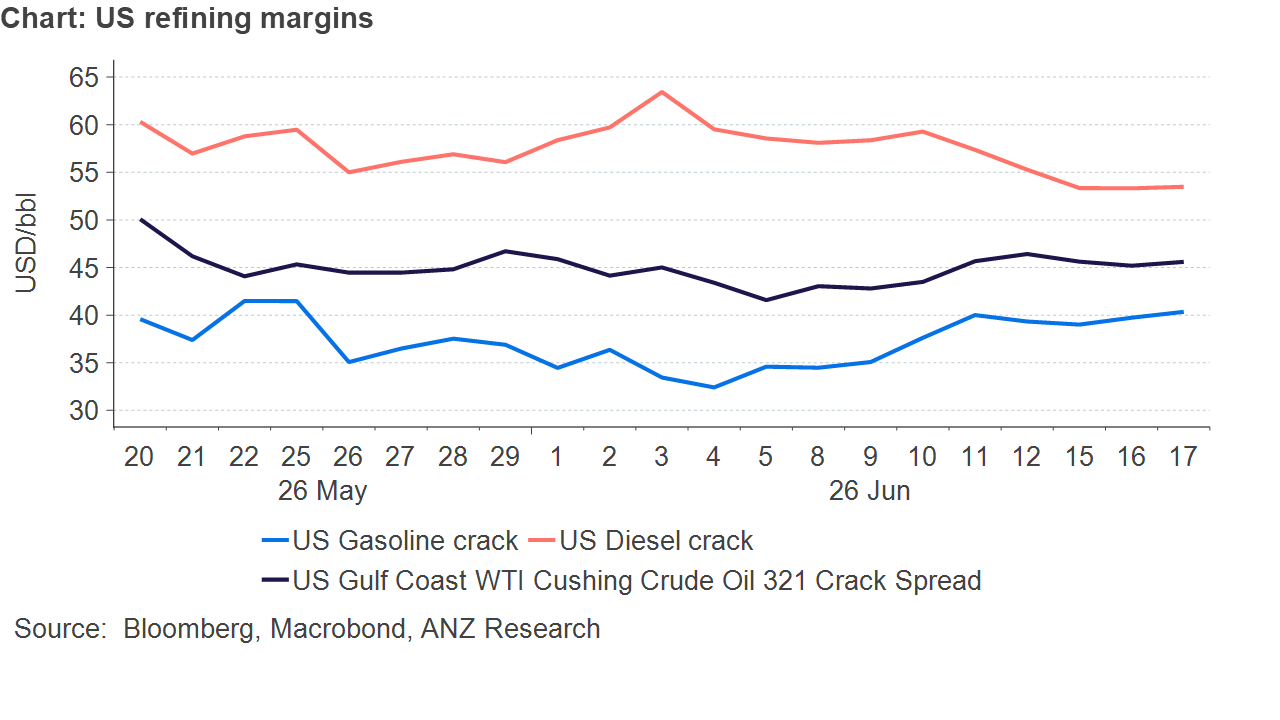

Chart of the Day

US refining margins have been edging higher in recent weeks, despite the slump in crude oil prices. Gasoline cracks are strengthening, backed by seasonal demand, low inventories, and ongoing supply constraints, while diesel cracks have softened but remain firm and well supported. We expect gasoline cracks to have more upside in the coming weeks as peak seasonal demand provides strong support. We also expect underlying diesel tightness to persist throughout the rest of the year, keeping cracks well-supported.

5in5 with ANZ Podcast