Commodities Wrap: Oil extends declines on expectations of a flood of supply

Wednesday 17 June, 2026

Summary

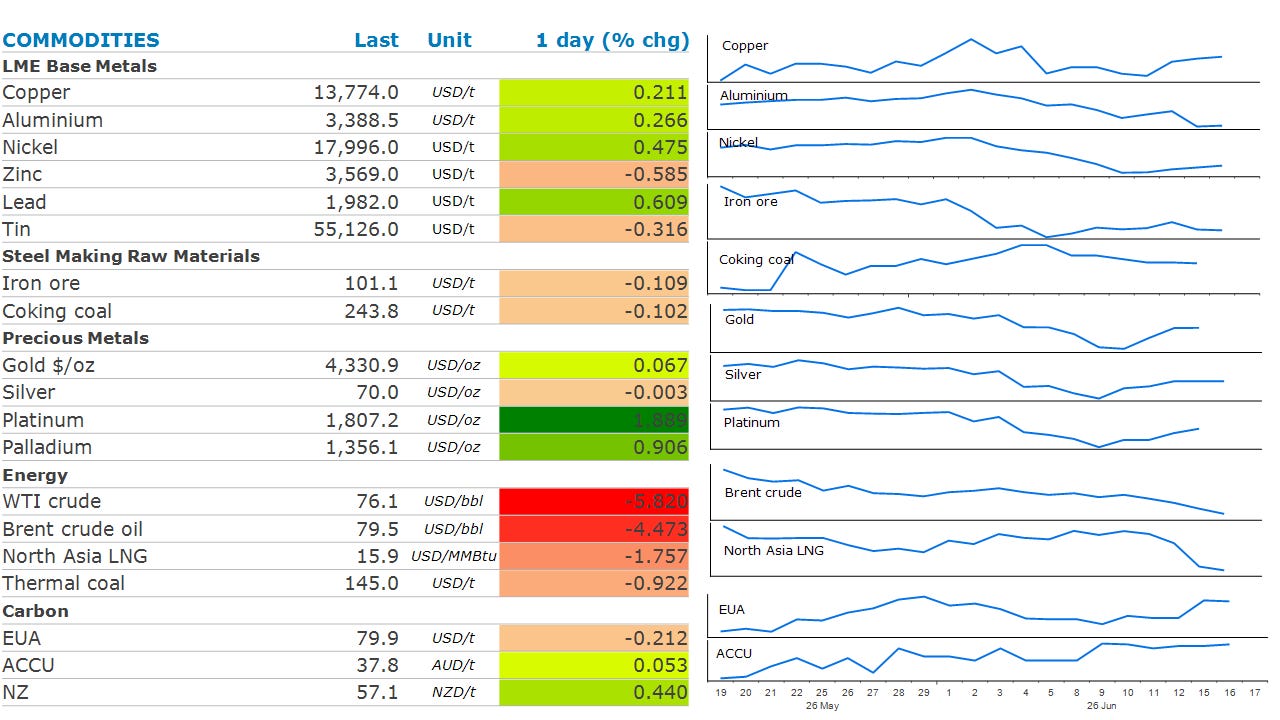

Expectations of rising supply from the Middle East pushed the energy sector lower. Precious and industrial metals gained as risk appetite improved.

Prices and commentary accurate as of 07:00 Sydney/05:00 Singapore/17:00(-1d) New York/22:00(-1d) London.

Ahead Today

Public holidays: None

Central bank speakers: RBA Assistant Governor Brad Jones Melbourne; ECB Sleijpens remarks

Economic data: Brazil rate decision; Eurozone CPI (11:00 Brussels / 10:00 UK / 19:00 AEDT), ECB wage tracker; Japan machinery orders, trade; Russia GDP, PPI; Singapore trade; South Africa CPI, retail sales; Sweden rate decision; UK CPI; US FOMC rate decision (14:00 NY / 19:00 UK / 04:00 AEDT); US retail sales, business inventories, pending home sales, mortgage applications

Commodities reports: IEA Oil Market Report (10:00 Paris / 09:00 UK / 18:00 AEDT); EIA weekly oil report (10:30 NY / 15:30 UK / 00:30 AEDT); Genscape ARA crude inventories (09:00 London / 04:00 NY / 13:00 AEDT)

Events: G7 Summit final day; FT Climate & Impact Summit London (through 18 Jun); Africa Energy Forum continues; Russia ASEAN summit; VivaTech Paris; SLB Investor Day

Market data: None

Listen to today’s 5in5 with ANZ podcast for more on the global economy and markets.

Market Commentary

Crude oil prices extended their decline, on expectations of a rebound in supply from the Middle East. Brent crude fell below USD80/bbl for the first time since late February ahead of the signing of a peace deal between the US and Iran which is expected to result in the reopening of the Strait of Hormuz. This has also seen regional crude benchmarks weaken in recent days. Spot prices for Dubai crude collapsed, pushing the discount for August contracts to around USD0.54/bbl. This is the first time it’s been in contango since late February. Nevertheless, many questions remain as to how the interim US-Iran deal will be implemented. Concerns over the safety of vessels remains high, while there is some doubt as to whether the chokepoint for a fifth of the world’s supply will remain toll-free. Shipping companies have indicated they need further details and assurances that the key waterway is free of mines before they resume transits on a large scale. Even then, the road to recovery will be challenging. We don’t expect supply from the Persian Gulf to be back to anything near pre-conflict levels until well into 2027.

European natural gas recorded further falls, as optimism grows over the revival of Middle East LNG supply. Bloomberg reported that Qatar, the top producer in the region, aims to rapidly boost LNG output once safe passage through the strait is restored. QatarEnergy has reportedly told buyers it aims to raise output to about 50% of capacity within a month. The remaining capacity will take years to fully restore following damage by Iranian missile strikes in March. North Asia LNG prices were also lower, although the losses were limited as other supply side issues persisted. Japan’s Inpex Corp expects industrial action will disrupt output at its LNG export plant in Australia.

Iron ore prices remained under pressure following week economic data. China’s fixed asset investment for January–May came in below expectations, down 4.1% y/y. This compares with -1.6% y/y in January–April. China’s crude steel output continues to fall, as the property sector shows no signs of recovery. Crude steel output in May fell 2.7% y/y to 84.36mt. That brings the year-to-date volumes to 415.53mt, down 3.9% y/y. Steel product output in May fell 2.8% y/y to 123.03mt. However, there is hope that India may offset some of this weakness. An industry gathering in Singapore has heard from Australian iron ore exporters that have said demand from the country is rising strongly. This is tied to a strong build-up in infrastructure spending.

Aluminium extended its slump as weaker-than-expected economic data dented sentiment. Retail sales declined 0.6% y/y in May – their worst drop since COVID-19 lockdowns in late 2022. This comes as the market prices-in a recovery of supply that has been disrupted by the Middle East conflict. Around 10% of global supplies have been impacted. However, some promising signs helped limit the damage across the rest of the base metal complex. Industrial production came in at 5.8%. The nickel market may be in for a period of volatility, as China warns of repercussions for Indonesia’s protectionist policies for the sector. The Financial Times reported that China warned Indonesia that up to USD20bn in planned future investments are at risk following Indonesia’s decision to slash production quotas for miners and establish a pricing mechanism that has raised the price of nickel ore.

Chart of the Day

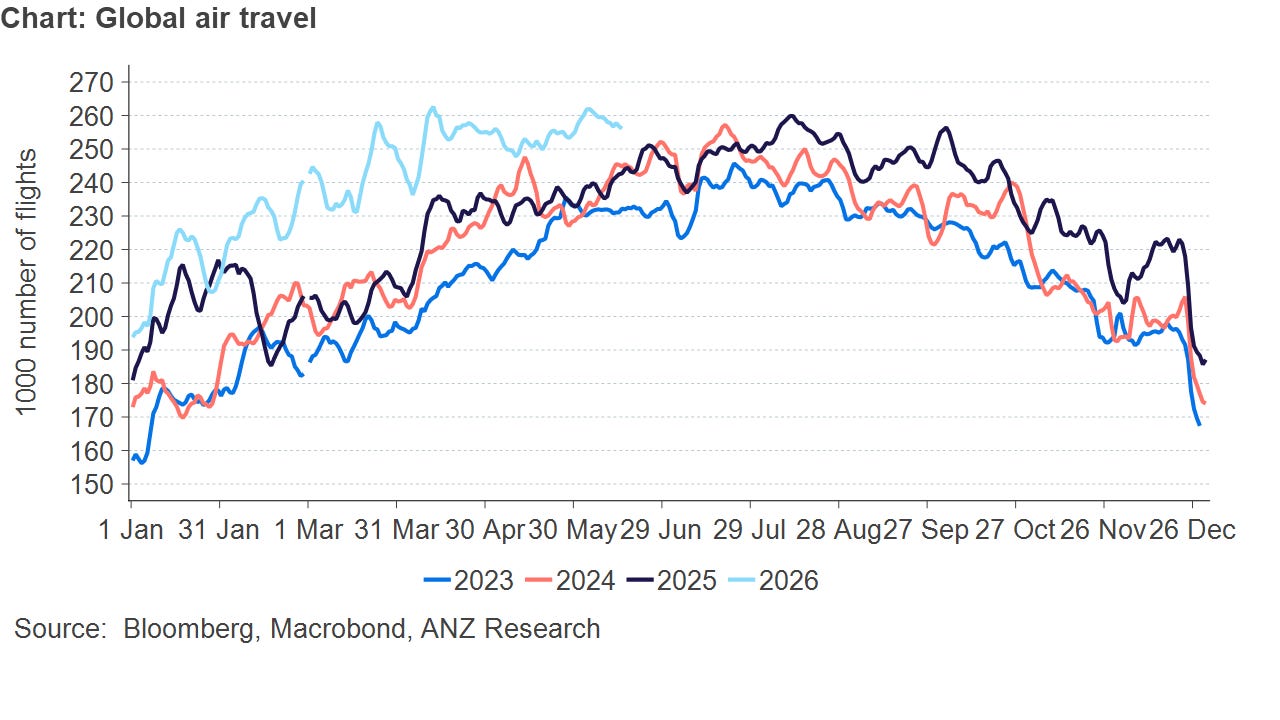

Global air travel has remained relatively robust, despite high oil prices pushing any airlines to reduce flights and raise ticket prices. The number of flights across the globe has remained on its normal seasonal uptick over the past three months. Fuel shortages have also been avoided due to refineries reconfiguring towards jet fuel.

5in5 with ANZ Podcast